Vancouver, Canada – TheNewswire - January 26, 2021 – Medgold Resources Corp. (TSXV:MED)|(FRA:1XD) is pleased to announce the completion of a positive Preliminary Economic Assessment (“PEA”) for the Barje gold deposit at its Tlamino Project, Serbia (“Barje”, “Tlamino”, the “Project”). The highlights of the PEA are as follows:

- Based on simple open-pit mining methods and the production of a flotation concentrate via conventional processing techniques, the pre-tax NPV of the Project, at a discount rate of 8%, is US$101M, its IRR 49%, and its operating margin 61%.

- A gold price of US$1500/oz and a silver price of US$16.50/oz was used in the study. At an approximate spot gold price of US$1,800/oz, the post-tax NPV of the Project, at a discount rate of 8%, is US$139M, and its IRR 69%.

It is now the intention of Medgold to pursue a program of infill drilling at Tlamino with the objective of upgrading the current Inferred Resource to the Indicated category, and the completion of a Pre-Feasibility Study thereafter. Drilling is expected to commence upon snow melt in Q1, 2021, further details of which will be provided in due course.

The key financial metrics of the Project are summarized in Table 1.

Table 1: Barje PEA Key Financial Metrics1

---------------------------------------

|Metric |Value|Units |

|-------------------------------------|

|Revenue |458 |US$M |

|-------------------------------------|

|Operating Cost |181 |US$M |

|-------------------------------------|

|Peak Funding Requirement|37 |US$M |

|-------------------------------------|

| | | |

|-------------------------------------|

|Project Capital Cost |74 |US$M |

|-------------------------------------|

|Free Cashflow |153 |US$M |

|-------------------------------------|

|LOM C1 Cash Cost |464 |US$/oz|

|-------------------------------------|

|LOM AISC |522 |US$/oz|

|-------------------------------------|

|Pre-Tax Project NPV8 |101 |US$M |

|-------------------------------------|

|Post-Tax Project NPV8 |86 |US$M |

|-------------------------------------|

|Pre-Tax Project IRR |49 |% |

|-------------------------------------|

|Post-Tax Project IRR |46 |% |

|-------------------------------------|

|Operating Margin |61 |% |

|-------------------------------------|

| | | |

|-------------------------------------|

|Payback Period |2 |years |

---------------------------------------

The PEA is preliminary in nature and is based on Inferred Mineral Resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as Mineral Reserves. As such there may be no certainty that the PEA will be realized. The study was undertaken by Addison Mining Services Ltd., Bara Consulting Ltd. and Reach Partners Limited, all of the United Kingdom. A Technical Report for the Project will be filed on http://www.sedar.com within 45 days.

Jeremy Crozier, President and CEO of Medgold, remarked that “the accomplishment of this highly positive Preliminary Economic Assessment - based entirely on conventional opening pit mining and processing techniques - is a critical success for Medgold. Together with the recent Option Agreement with Fortuna Silver Mines to acquire full ownership and management control of the Project, Medgold is now placed to unlock further value in Tlamino via the completion of infill drilling and a Pre-Feasibility Study - with the goals of further demonstrating the robust self-standing economics of the Project, and ultimately the achievement of mine permitting. Addison Mining Services Ltd., Bara Consulting Ltd. and Reach Partners Limited are thanked for their diligence in the preparation of the PEA”.

Basis of Preliminary Economic Assessment

Scoping-level design and preliminary economic analysis thereof was undertaken for the Barje deposit of the Tlamino Project. The Mineral Resource Estimate for Barje as announced on January 30, 2020 has been updated in accordance with the metallurgical testwork and mining parameters identified during the course of the current study. An updated Inferred Mineral Resource of approximately 7.1 Mt at 2.5 g/t Au and 38 g/t Ag, containing approximately 570,000 oz of Au and 8.8 Moz of Ag is herein stated and has been used as a basis for this PEA.

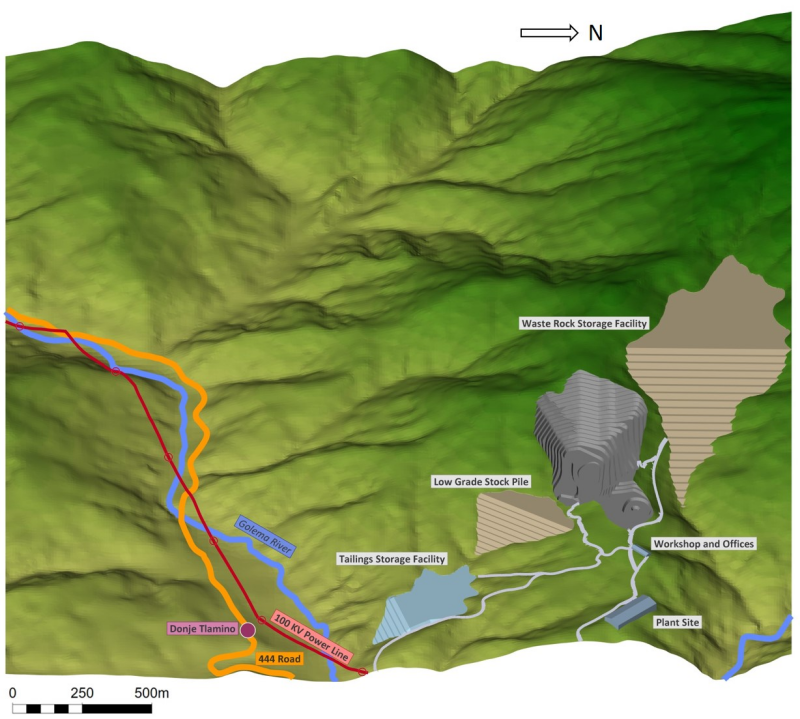

Mining via open pit methods using a conventional truck and shovel fleet is contemplated, delivering approximately 600,000 tpa of two Run of Mine (“ROM”) material types - High-Grade Breccia (“HG_BX”) and Low-Grade Schist (“LG_Sch”) - to stockpile for processing, with a life-of-mine stripping ratio of approximately 4:1. On site mineral processing is via grinding and flotation to a bulk Au-Ag bearing sulphide concentrate for sale to potential offtake customers in Asia. Preliminary economic analysis has been performed in accordance with the preliminary mine design and schedule, metallurgical testing, and concentrate payability analysis developed in the study, and the estimates and analyses therein have been prepared to scoping level (+-30%). Oxidized material from the Mineral Resource was not considered by the PEA, and the nearby prospects at Liska and Karamanica were similarly omitted. A preliminary site layout, subject to further study, permitting and land access is shown in Figure 1. Key project parameters are presented in Table 2.

6

Click Image To View Full Size

Figure 1: Preliminary Site Layout, Barje (looking west)

Table 2: Summary of Project Parameters

------------------------------------------------

|Parameter |Value|Units |

|----------------------------------------------|

|LOM Production Rate |710 |ktpa |

|----------------------------------------------|

|Waste Mining Rate |3,310|ktpa |

|----------------------------------------------|

|LOM Average Strip Ratio |4:1 |Waste t:ROM t |

|----------------------------------------------|

|Average Mined Gold Grade|2.6 |g/t |

|----------------------------------------------|

|Total Mined Gold |390 |koz |

|----------------------------------------------|

|Total Mined Silver |4,022|koz |

|----------------------------------------------|

|Cut-off Grade -HG_BX |0.6 |g/t AuEq |

|----------------------------------------------|

|Cut-off Grade -LG_Sch |1.14 |g/t AuEq |

|----------------------------------------------|

|LOM |8 |years |

|----------------------------------------------|

|Mining Cost - OPEX |2.30 |US$/t mined |

|----------------------------------------------|

|Process Cost - OPEX |11.50|US$/t processed|

|----------------------------------------------|

|Base Case Au Price |1,500|US$/oz |

|----------------------------------------------|

|Base Case Ag Price |16.50|US$/oz |

------------------------------------------------

Mining

The Barje deposit is relatively flat-lying and situated beneath shallow to medium-depth overburden. While mining via both open pit and underground techniques were initially considered, an open pit method was ultimately selected for the PEA on account of the overall low volume of waste and the generally low RQD of both waste and ore material. The PEA contemplates application of open pit mining methods using hydraulic excavators and wheel loaders charging articulated dump trucks for haulage of both waste and ROM material. Mining activities will be performed on a contractor basis, and include free-digging of weathered material, and drilling and blasting of fresh rock. Pre-production mining includes removal and stockpiling of topsoil is also assumed.

Mining is expected to be completed over four pit stages with an active life of mine (“LOM”) of approximately eight years, followed by a further two years of production from stockpile reclamation. Pit and schedule optimizations prioritize mining and processing of HG_BX material where possible, with LG_Sch material stockpiled and processed periodically throughout the LOM. Mining parameters are summarized in Table 3.

Table 3: Summary of Mining Parameters

---------------------------------------------------

|LOM Summary |Total|Units |

|-------------------------------------------------|

|Total Rock |31.7 |Mt |

|-------------------------------------------------|

|Total Waste |26.0 |Mt |

|-------------------------------------------------|

|Total ROM |5.69 |Mt |

|-------------------------------------------------|

|LOM Average Strip Ratio |4:1 |Waste t:ROM t|

|-------------------------------------------------|

|Plant Feed (All) |5.69 |Mt |

|-------------------------------------------------|

| |2.62 |g/t Au |

|-------------------------------------------------|

| |38.9 |g/t Ag |

|-------------------------------------------------|

|Plant Feed (HG_BX) |3.57 |Mt |

|-------------------------------------------------|

| |3.43 |Au g/t |

|-------------------------------------------------|

| |56.1 |Ag g/t |

|-------------------------------------------------|

|Plant Feed (LG_Sch) |2.11 |Mt |

|-------------------------------------------------|

| |1.25 |Au g/t |

|-------------------------------------------------|

| |9.9 |Ag g/t |

|-------------------------------------------------|

|LOM |8 |years |

|-------------------------------------------------|

|Stockpile Reclaim |2 |years |

|-------------------------------------------------|

|Total |10 |years |

|-------------------------------------------------|

|Peak Production Total Rock |10.6 |Mt/year |

|-------------------------------------------------|

|Peak Production Waste |10.0 |Mt/year |

|-------------------------------------------------|

|Peak Production ROM |1.4 |Mt/year |

|-------------------------------------------------|

|Average Production Total Rock|4.0 |Mt/year |

|-------------------------------------------------|

|Average Production Waste |3.3 |Mt/year |

|-------------------------------------------------|

|Average Production ROM |0.7 |Mt/year |

---------------------------------------------------

Processing

Test work on Barje samples reported by Medgold on October 28, 2020 demonstrated the production of a flotation concentrate at a primary grind of 75 µm grading 48.9 g/t Au and 824 g/t Ag with recoveries to concentrate of 83.4% for gold and 82.4% for silver from a composite sample representing the HG_BX material. A second composite sample representing the LG_Sch material produced a flotation concentrate at a similar grind grading 24.4 g/t Au and 238 g/t Ag with recoveries to concentrate of 71.2% for gold and 79.2% for silver. Laboratory test work shows that the same grind size and flotation parameters are applicable to both rock types and can result in commercially viable concentrates. These results were incorporated into the PEA and were used in re-assessment of the Mineral Resource Estimate.

A flowsheet contemplating crushing, grinding, and rougher plus cleaner flotation to a bulk Au-Ag concentrate has been developed based on the metallurgical test program. It is envisaged that the two ROM material types be processed in the same concentrator, but at different times, i.e. on a campaign basis, in order to maximize revenue from the HG material.

The PEA provides that ROM material is hauled by trucks and tipped on a storage and blending stockpile. Ball milling with feed prepared by three-stage crushing and screening is further assumed as it is deemed to represent a robust option for this material type. A rougher flotation stage followed by two stages of cleaner flotation are sufficient to produce acceptable concentrate of the previously reported specification. Concentrates are dewatered by means of a pressure filter, with concentrate filter cake stored and blended before transport by road and sea for processing at toll facilities in Asia.

Tailings are densified in a high-rate thickener before final dewatering by means of a pressure filter before storage in a dry-stack type Tailings Storage Facility (“TSF”), thus improving the geotechnical properties of the TSF and maximizing recycling of process water. Key processing parameters are presented in Table 4.

Table 4: Summary of Mineral Processing Parameters

------------------------------------------------------

|Parameter |Value|Units |

|----------------------------------------------------|

|Flotation Throughput |600 |ktpa |

|----------------------------------------------------|

|Au Recovery HG_BX |85.8 |% |

|----------------------------------------------------|

|Ag Recovery HG_BX |84.3 |% |

|----------------------------------------------------|

|Au Recovery LG_Sch |76.5 |% |

|----------------------------------------------------|

|Ag Recovery LG_Sch |84.3 |% |

|----------------------------------------------------|

|Mass Pull |5 |% |

|----------------------------------------------------|

|Au grade HG conc |49 |g/t |

|----------------------------------------------------|

|Ag grade HG conc |824 |g/t |

|----------------------------------------------------|

|Au grade LG conc |24 |g/t |

|----------------------------------------------------|

|Ag grade LG conc |238 |g/t |

|----------------------------------------------------|

|Recovered Au |390 |koz |

|----------------------------------------------------|

|Recovered Ag |4,022|koz |

|----------------------------------------------------|

|Payability– HG conc |75 |% |

|----------------------------------------------------|

|Payability– LG conc |40 |% |

|----------------------------------------------------|

|Flotation Process Costs - OPEX|11.50|US$/processed t|

|----------------------------------------------------|

|G&A |5.80 |US$/processed t|

|----------------------------------------------------|

|Concentrate Transport Cost |3.24 |US$/processed t|

------------------------------------------------------

Capital Costs

The Project is well-served by existing infrastructure including sealed roads and a high voltage power line adjacent to the property. Capital costs for mine development, mine infrastructure, processing plant, and surface infrastructure including mine offices, control, plant building, common workshop and stores, changehouse, water, powerline and substation, and earthworks including tailings, roads and platforms were estimated based on current designs and quotes from recent comparable projects by Bara Consulting.

Plant capital provides for the design and construction of a 600,000 tpa flotation plant including crushing, grinding, froth flotation, concentrate and tailings handling facilities including filtration of tailings for dry stacking. Infrastructure includes for mine support infrastructure, plant infrastructure, dry stack tailings storage facility, power (including backup 35 kV line), water and internal roads. A summary is presented in Table 5. Estimates for closure were also assessed during the ESIA review process.

Table 5: Capital Cost Estimates

-----------------------------------------------

|Description |Value |Units|Cost |

|---------------------------------------------|

|Mine Development |3.25 |Mt |US$7.5M |

|---------------------------------------------|

|Process Plant |600,000|tpa |US$34.6M|

|---------------------------------------------|

|Surface Infrastructure| | |US$14.0M|

|---------------------------------------------|

|Indirect Costs |15 |% |US$8.4M |

|---------------------------------------------|

|Contingency |15 |% |US$9.7M |

|---------------------------------------------|

|Total | | |US$74.2M|

-----------------------------------------------

Operating Costs

A high-level breakdown of operating costs was developed based on current designs and quotes from recent similar projects by Bara Consulting. Mine operating costs include ore mining and waste mining at US$2.30/t, plus a stockpile reclaim cost for LG material of US$1/t equating to US$0.50/ROM tonne. Process costs include crushing, grinding, flotation, concentrate handling and tailings handling (including filtration) for 600,000 tpa flotation feed. G&A includes on-mine administration and general costs. Concentrate transport is costed for delivery of concentrate CIF to customers in China. Details are presented in Table 6 below.

Table 6: Operating Cost Estimates

--------------------------------------------

|Description |Units|Cost/Unit|

|------------------------------------------|

|Mining |

|------------------------------------------|

|Mining Cost - ROM |t |US$2.80 |

|------------------------------------------|

|Mining Cost - Waste |t |US$2.30 |

|------------------------------------------|

|Processing |

|------------------------------------------|

|Processing |t |US$11.50 |

|------------------------------------------|

|Conc Transport (Per ROM t)|t |US$3.24 |

|------------------------------------------|

|G&A |t |US$5.80 |

--------------------------------------------

Economics and Sensitivities

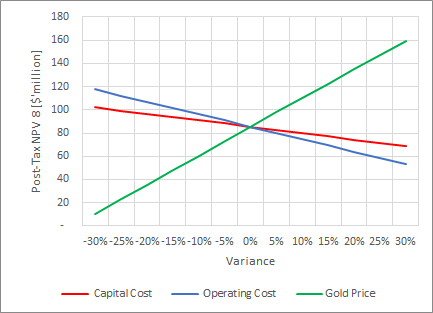

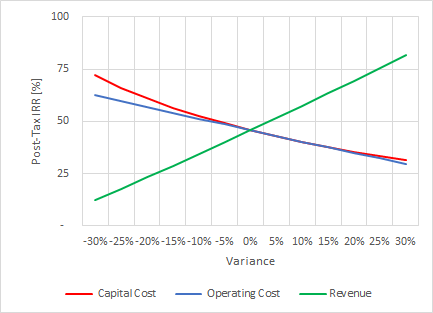

The post-tax NPV of the Project, at a discount rate of 8%, is US$86M, with an IRR of 46%, and an operating margin of 61%. Up-front capital is US$74M with payback achieved in two years. Life of mine C1 cash costs are US$464/oz Au, and life of mine AISC are US$522/oz Au. Sensitivity analysis of key capital and operating cost parameters, and gold price indicates significant upside potential to the project are shown in Figure 2. The Project was demonstrated to be most sensitive to variance in gold price, and least sensitive to variances in capital cost. Specific post-tax NPV and IRR sensitivity ranges are presented in Table 7.

Table 7 NPV and IRR sensitivities, Barje Prospect

--------------------------------------------------------------

|Variance|Gold |NPV |IRR|Capital|NPV |IRR|Operating|NPV |IRR|

| |Price |(8%)| |Cost |(8%)| |Cost |(8%)| |

| |US$/oz| | |(US$M) | | |US$/t | | |

|------------------------------------------------------------|

|-30% |1050 |10 |12 |52 |102 |72 |24 |118 |63 |

|------------------------------------------------------------|

|-25% |1125 |23 |18 |56 |99 |66 |26 |112 |60 |

|------------------------------------------------------------|

|-20% |1200 |36 |23 |59 |97 |61 |27 |107 |57 |

|------------------------------------------------------------|

|-15% |1275 |48 |29 |63 |94 |57 |29 |102 |54 |

|------------------------------------------------------------|

|-10% |1350 |61 |34 |67 |91 |53 |31 |96 |51 |

|------------------------------------------------------------|

|-5% |1425 |73 |40 |70 |88 |49 |32 |91 |49 |

|------------------------------------------------------------|

|0% |1500 |86 |46 |74 |86 |46 |34 |86 |46 |

|------------------------------------------------------------|

|5% |1575 |98 |52 |78 |83 |43 |36 |80 |43 |

|------------------------------------------------------------|

|10% |1650 |110 |57 |81 |80 |40 |37 |75 |40 |

|------------------------------------------------------------|

|15% |1725 |123 |63 |85 |77 |38 |39 |69 |38 |

|------------------------------------------------------------|

|20% |1800 |135 |69 |89 |74 |36 |41 |64 |35 |

|------------------------------------------------------------|

|25% |1875 |147 |76 |93 |71 |34 |43 |59 |32 |

|------------------------------------------------------------|

|30% |1950 |160 |82 |96 |69 |32 |44 |53 |30 |

--------------------------------------------------------------

Click Image To View Full Size

Click Image To View Full Size

Figure 1-2- Post-Tax NPV and IRR Sensitivity, Barje Deposit

Mineral Resources

Mineral Resources, reported in accordance with National Instrument 43-101, Standards of Disclosure for Mineral Projects, (“NI 43-101”) and the Canadian Institute of Mining, Metallurgy and Petroleum (CIM) Definition Standards, have been re-estimated for the Barje prospect of the Tlamino Project incorporating updated metallurgical testwork and mining parameters identified during the PEA. No Mineral Resources for other prospects within the Tlamino Project (Liska, Karamanica) have as yet been declared.

The estimated Mineral Resource for Barje, using various cut-off grades for their respective material types, is approximately 7.1 Mt at 2.5 g/t Au and 38 g/t Ag in the Inferred category, and containing 570,000 oz of Au and 8.8 Moz of Ag. This equates to approximately 2.9 g/t AuEq or 670,000 oz AuEq. It is the opinion of the Qualified Person for the Mineral Resource Estimate that all elements included in the Au Equivalent calculation (gold and silver) have a reasonable prospect of being recovered and sold.

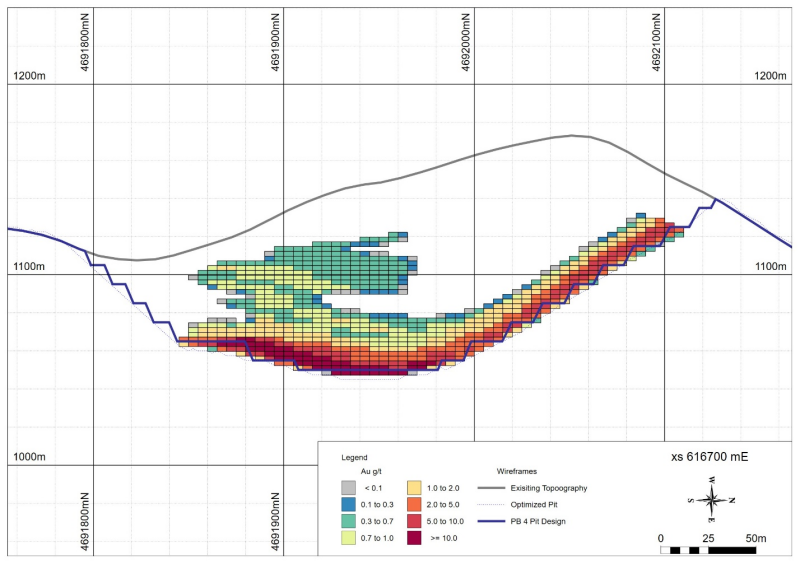

The updated Mineral Resource Estimate has an effective date of January 7, 2021 and supersedes the previous initial Mineral Resource Estimate announced on January 30, 2020; there has, however, been no material change to the estimate in terms of tonnage, grade and contained metal. See Table 8 for further information relating to the updated Mineral Resource Estimate. A north-south cross-section illustrating the optimized Barje pit and block model is shown in Figure 3.

Figure 3: north-south cross-section illustrating the optimized Barje pit and block model.

Click Image To View Full Size

No estimates of Mineral Reserves have been completed. Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability. The estimate of Mineral Resources may be materially affected by environmental, permitting, legal, title, taxation, socio-political, marketing, or other relevant issues.

The Mineral Resources extend from surface to a depth of approximately 110 m, are laterally extensive over an area of approximately 600 m from east to west and approximately 350 m north to south. The thickness of resource mineralization ranges from approximately 10 to 40 m with some isolated thinner areas. It is closed by bounding faults to the north and south and by drilling to the east and west. There remains some possibility of identifying additional mineralization via infill drilling in areas where the model is currently interpreted to pinch and in which data are sparse, and in the northwest corner of the area of mineralization.

Table 8: Mineral Resource Estimate, Barje Prospect

--------------------------------------------------------------

| |AuEq |Au |Ag |

|------------------------------------------------------------|

|Tonnes |Density|g/t| Contained|g/t|Contained|g/t|Contained|

| | | |oz | |oz | |oz |

|------------------------------------------------------------|

|Total Inferred Resources |

|------------------------------------------------------------|

|7,100,000|2.7 |2.9|670,000 |2.5|570,000 |38 |8,800,000|

|------------------------------------------------------------|

|Including |

|------------------------------------------------------------|

|High Grade Breccia |

|------------------------------------------------------------|

|3,200,000|2.8 |4.7|470,000 |3.9|400,000 |65 |6,700,000|

|------------------------------------------------------------|

|Low Grade Schist |

|------------------------------------------------------------|

|2,400,000|2.7 |1.2|96,000 |1.1|88,000 |8.4|650,000 |

|------------------------------------------------------------|

|Partially Oxidized Material |

|------------------------------------------------------------|

|1,500,000|2.5 |2.1|100,000 |1.7|87,000 |29 |1,400,000|

--------------------------------------------------------------

Notes to the Mineral Resource Estimate:

1.The independent Qualified Person for the Mineral Resource Estimate, as defined by NI 43-101, is Mr. Richard Siddle, MSc, MAIG, of Addison Mining Services Ltd since November 2014. The effective date of the Mineral Resource Estimate is January 07 2021.

2.These Mineral Resources are not Mineral Reserves as they do not have demonstrated economic viability. The quantity and grade of reported Inferred Resources in this Mineral Resource Estimate are uncertain in nature and there has been insufficient exploration to define these Inferred Resources as Indicated or Measured, however it is reasonably expected that the majority of Inferred Mineral Resources could be upgraded to Indicated Mineral Resources with continued exploration. Additional drilling is however required to increase the confidence in the Mineral Resource; increased levels of information brought about by further drilling may serve to either increase or decrease the Mineral Resources.

3.Mineral Resources reported in the above table are presented as undiluted and in-situ for an open-pit scenario and are considered to have reasonable prospects for economic extraction. The Mineral Resources constrained by open pit optimization.

4.Break even cut-off grades were estimated for each material type of 0.6 g/t, 0.8g/t and 0.5 g/t AuEg for the High Grade Breccia, Low Grade Schist and Partially Oxidized materials respectively, these cut-off grades were used in Resource Reporting. The cut-off grades were calculated on the basis of the following assumptions: a gold price of US$1500/oz, a silver price of US$16.5/oz, mining costs of US$2.3/t, processing costs including tailings disposal of US$10/t for sulphide rock and US$12/t for oxide, G&A costs of US$4/ROMt and transport costs of US$2/ROMt.

5.Per metallurgical test work completed to date, recovery to concentrate after flotation of 85.8% for gold and 84.3% for silver were used for the High Grade Breccia material with 75% payability. For the Low Grade Schist recoveries used were 76.5% for gold and 82.7% for silver with 60% payability. For the Partially Oxidized material 80% recovery via leaching for gold and silver was assumed with 98% payability. 5% gross royalty was applied to both metals.

6.Geological and block models for the Mineral Resource Estimate used data from 33 surface drillholes performed by Medgold in 2018 and 2019; data from four drillholes completed by Avala Resources Ltd., a prior operator, were used to constrain the model though they did not intercept significant mineralization. The drill database was validated prior to resource estimation and QA/QC checks were made using industry-standard control charts for blanks, core duplicates and commercial certified reference material inserted into assay batches by Medgold and by comparison of umpire assays performed at a second laboratory. No QA/QC was possible on the data relating to the drilling by Avala.

7.The geological model as applied to the Mineral Resource Estimate comprises two mineralized domains, a shallowly inclined high-grade hydrothermal breccia unit and a lower-grade schist unit immediately overlying the hydrothermal breccia. Individual wireframes were created for each domain. Weathering domains of fresh and partially oxidized material were defined within the two mineralized domains.

8.The block model was prepared using Micromine version 2020, Services Pack 1, A 10 m x 10 m x 4 m block model was created with sub-blocks of minimum 2 m x 2 m x 2 m on domain boundaries. Grade estimation from drillhole data was carried out for Au, Ag, As, Cu, Pb, Zn, Fe, S using Ordinary Kriging and was validated by comparison of input and output statistics, kriging neighbourhood analysis and by inspection of the assay data and block model in cross section. A gold equivalent (AuEq) grade was calculated for each block using the formula AuEq = ((Ag g/t) x 0.011)) + (Au g/t) for the High Grade Breccia and Partially Oxidized materials and AuEq = ((Ag g/t) x 0.012)) + (Au g/t) for the Low Grade Schist.

9.Bulk density values were calculated for each block of the model based on a broad linear relationship observed between 152 measured bulk density values within the mineralized domains and the assayed values of As, Cu, Fe, S, Pb and Zn. Blocks within the partially oxidized material were assigned a single bulk density value of 2.54 g/cm3.

10.Estimates in the above table have been rounded to two significant figures.

11.CIM Definition Standards for Mineral Resources have been followed.

12.The independent Qualified Person for Resources is not aware of any additional known environmental, permitting, legal, title, taxation, socio-political, marketing, or other relevant issues that could materially affect the Mineral Resource Estimate.

Future Work

Recommendations include infill drilling to support the conversion of Inferred to Indicated Resources, and field programs in support of a Pre-Feasibility Study on the Barje Deposit. This work would include additional geotechnical and hydrogeological investigation, additional metallurgical testing and commencement of environmental baseline data collection including air, water, soil, fauna and flora studies.

The Tlamino Project

The Tlamino Project covers an area of approximately 200km2 in southern Serbia and is held by Medgold under two exploration licenses. Outcropping mineralization was first observed at the Barje Prospect by Yugoslav State agencies in the 1950s and 1960s when a short adit was opened but no drilling was carried out. The prospect was then held by private and public companies between approximately 2005 and 2012 during which time limited drilling failed to intersect significant mineralization.

Medgold conducted mapping, surface sampling and geophysics (IP) followed by diamond drilling at the Barje Prospect in 2018 and 2019, all fully funded by Fortuna Silver Mines Inc. (“Fortuna”) under the terms of an Option Agreement announced on May 1, 2017. The drilling intersected gold mineralization in a shallowly inclined body of hydrothermal breccia below altered schist (as announced on March 21, 2019). The Inferred Mineral Resource at the Barje Prospect extends from surface to a depth of approximately 110m as a shallowly inclined zone over an area of approximately 600 m x 350 m. The true thickness of mineralization generally ranges between 10 m to 40 m.

On January 7, 2021 Medgold announced that, subject to stock exchange approval, it has entered into a definitive Option Agreement (the “Agreement”) with Fortuna to acquire Fortuna’s 51% interest in the Project. The terms of the Agreement provide Medgold with an exclusive option (the “Option”) to purchase Fortuna’s interest in the Project for a cash consideration of US$ 3.468 million. The Option is valid for three years and is exercisable (i) at any time at the election of Medgold prior to the expiry of the term of the Option; or (ii) at the date of completion of a sale by Medgold of a 100% interest in the Project to a third party; or (iii) at the date of completion of a merger between Medgold and a third party, whichever arises soonest.

In the event that Medgold completes a sale of the Project or corporate merger during the term of the Option and receives consideration in excess of US$ 8.84 million (the “Sale Consideration”), Medgold will pay to Fortuna an asset sale bonus equal to 10.2% of any amount in excess of the Sale Consideration, less all of Medgold’s costs related to the sale or corporate merger.

Qualified Persons and Data Verification

Mr. Thomas Sant, FGS, CGeol, EurGeol, Consultant Exploration Manager for Medgold and Qualified Person as defined by NI 43-101, has reviewed and approved the scientific and technical content of this news release. Mr. Sant is not independent of the Company.

The independent Qualified Persons as defined by NI 43-101, are Mr. Richard Siddle, MAIG, of Addison Mining Services Ltd for Mineral Resources; Dr. Matthew Randall, FIMMM, of Axe Valley Mining Consultants Ltd for Mining; Mr. Ian Jackson, FIMMM, of Bara Consulting for Mineral Processing, and Dr. Andrew Bamber, MCIM, of Bara Consulting Ltd for Economic Analysis.

About Medgold Resources Corp.

Medgold is a TSX-V listed, gold exploration company targeting early-stage properties in the Balkan region. Run by an experienced management team with a successful track-record of building value in resource companies, Medgold is focused on growth through fast-paced exploration and resource definition in the prospective and under-explored Balkan region.

Additional information on Medgold can be found on the Company’s website at www.medgoldresources.com and by reviewing the Company’s page on SEDAR at www.sedar.com.

ON BEHALF OF THE BOARD

Jeremy Crozier, President and CEO

For Further Information, Contact:

President and CEO

Jeremy Crozier (Vancouver), +1 604 801 5432, info@medgoldresources.com

Neither the TSX Venture Exchange nor the Investment Industry Regulatory Organization of Canada accepts responsibility for the adequacy or accuracy of this release.

Forward-looking statements

Certain statements contained in this news release constitute forward-looking statements within the meaning of Canadian securities legislation. All statements included herein, other than statements of historical fact, are forward-looking statements and include, without limitation, statements about the potential acquisition by the Company of Fortuna’s interest in the Tlamino Project, and the mineral resource estimate and PEA for the Tlamino Project. Often, but not always, these forward looking statements can be identified by the use of words such as “estimate”, “estimates”, “estimated”, “potential”, “open”, “future”, “assumed”, “projected”, “used”, “detailed”, “has been”, “gain”, “upgraded”, “offset”, “limited”, “contained”, “reflecting”, “containing”, “remaining”, “to be”, “periodically”, or statements that events, “could” or “should” occur or be achieved and similar expressions, including negative variations.

Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of the Company to be materially different from any results, performance or achievements expressed or implied by forward-looking statements. Such uncertainties and factors include, among others, whether the Company will obtain stock exchange approval to the Option, and ultimately acquire Fortuna’s interest in the Tlamino Project; the uncertainties inherent in the PEA and the estimation of mineral resources; changes in general economic conditions and financial markets; the Company or any joint venture partner not having the financial ability to meet its exploration and development goals; risks associated with the results of exploration and development activities, estimation of mineral resources and the geology, grade and continuity of mineral deposits; unanticipated costs and expenses; and such other risks detailed from time to time in the Company’s quarterly and annual filings with securities regulators and available under the Company’s profile on SEDAR at www.sedar.com. Although the Company has attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward-looking statements, there may be other factors that cause actions, events or results to differ from those anticipated, estimated or intended.

Forward-looking statements contained herein are based on the assumptions, beliefs, expectations and opinions of management, including but not limited to: the Company will obtain stock exchange approval to the Option; the accuracy of the PEA and the mineral resource estimate for the Tlamino Project; that the Company’s stated goals and planned exploration and development activities will be achieved; that there will be no material adverse change affecting the Company or its properties; and such other assumptions as set out herein. Forward-looking statements are made as of the date hereof and the Company disclaims any obligation to update any forward-looking statements, whether as a result of new information, future events or results or otherwise, except as required by law. There can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, investors should not place undue reliance on forward-looking statements.

Unless otherwise stated, all tonnes referenced in this News Release are metric, and ounces are troy ounces.